Memorandum

City of Lawrence

City Manager’s Office

|

TO: |

David L. Corliss, City Manager |

|

CC: |

Diane Stoddard, Assistant City Manager |

|

FROM: |

Britt Crum-Cano, Economic Development Coordinator |

|

DATE: |

January 27, 2015 |

|

RE: |

Technical Report: NRA and IRB request for 705 Massachusetts Street |

Executive Summary

The Eldridge Hotel LLC is proposing the expansion of the existing hotel (705 Massachusetts Street) onto the vacant lot located next to the hotel at 705 Massachusetts Street. To assist with the expansion, the company is asking for a 15-year, 95% NRA rebate and IRB financing for a sales tax exemption on construction materials.

Analysis shows that for a 10-year or 15-year NRA period at the 95% rebate level, the project will more than double the amount of property tax currently being collected. The below table shows cumulative projected property and sales tax collections for the project, assuming a15-year, 95% NRA. (Refer to Addendum E for projections by year.)

|

Projected Property & Sales Tax Revenues |

|||

|

|

10 Years (2017-2026) |

15 Years (2017-2031) |

20 Years (2017-2026 |

|

Property Tax Revenues |

$116,952 |

$181,696 |

$1,086,806 |

|

Sales Tax Revenues |

$1,819,300 |

$2,924,393 |

$4,144,504 |

|

Total Tax Projected |

$1,936,251 |

$3,106,088 |

$5,231,311 |

The City, County, and School District individually considers their participation in an NRA and has the discretion to determine the rebate percentage and duration of the NRA. The rebate level and duration period should be a topic of discussion for PIRC and the governing bodies.

Project Overview

Eldridge Hotel, LLC, (project Owner) is proposing the expansion of the existing Eldridge Hotel located at 701 Massachusetts Street by developing the vacant parcel, located next to the existing hotel, at 705 Massachusetts Street.

Located along the historic Downtown Massachusetts Street corridor in Lawrence, Kansas, the Eldridge building has been part of community history and culture since 1855. The hotel underwent a complete restoration in 2005 and features historic accommodations including, 48 guest suites, a full-service restaurant and lounge, and banquet room space.

The expansion project would add approximately 54 new guest rooms and provide approximate 5,000 feet for additional meeting/banquet room space, hotel kitchen expansion, and restaurant and bar concept.

Request for NRA Assistance

A Request Letter and Incentives Application were received January 15, 2015 from Eldridge Hotel, LLC requesting a 15-year, 95% Neighborhood Revitalization Area (NRA) Industrial Revenue Bond (IRB) financing in order to receive a sales tax exemption on construction materials.

The following presents details and analytical results associated with this request.

Neighborhood Revitalization Area (NRA)

Description of NRA and Purpose

The NRA is one of several economic development tools utilized by municipalities to promote economic growth through neighborhood enhancement. Authorized by the state, NRAs are intended to encourage the reinvestment and revitalization of properties which in turn have a positive economic effect upon a neighborhood and the City in general. The use of an NRA is particularly applicable for use in areas where rehabilitation, conservation, or redevelopment is necessary to protect the public health, safety or welfare of the residents of the City.

Typically, a percentage of the incremental increased value in property taxes (due to improvements) is rebated back to the developer/applicant over a period of time to help offset redevelopment costs and make the project financially feasible.

NRA Project Eligibility

Project eligibility for NRA consideration is governed by both State (KSA 12-17,114 et seq.) and City policy.

State Requirements

|

Statutory Criteria |

Governing Body determines that rehabilitation, conservation or redevelopment of the area is necessary to protect the public health, safety or welfare of residents and the proposed project meets at least one of the below criteria: |

|

|

|

1 |

An area in which there is a predominance of buildings or improvements which by reason of dilapidation, deterioration, obsolescence, inadequate provision of ventilation , light, air or open spaces, high density of population and overcrowding, the existence of conditions which endanger life or property by fire and other causes or a combination of such factors, is conductive to ill health, transmission of disease, infant mortality, juvenile delinquency or crime and which is detrimental to the public health, safety or welfare. |

Health & Safety Need |

|

|

2 |

An area which by reason of the presence of a substantial number of deteriorated or deteriorating structures, defective or inadequate streets, incompatible land uses relationships, faulty lot layout in relation to size, adequacy, accessibility or usefulness, unsanitary or unsafe conditions deterioration of site or other improvements, diversity of ownership, tax, or special assessment delinquency exceeding the actual value of the land, defective or unusual conditions of title, or the existence of conditions which endanger life or property by fire and other causes or a combination of such factions substantially impairs or arrests the sound growth of a municipality, retards the provision of housing accommodations, or constitutes an economic or social liability and is detrimental to the public health, safety or welfare in its present condition and use. |

Economic Need |

|

|

3 |

An area in which there is a predominance of buildings or improvements that should be preserved or restored to productive use because of age, history, architecture or significance should be preserved or restored to productive use. |

Preservation of Community/Historical Asset |

|

Conclusion—State Eligibility:

Staff believes the project as proposed will meet State NRA eligibility criteria due to the deterioration of the site or other improvements. The site previously had a structure on it, which staff believes was destroyed by fire in the early 1970s. The site has been vacant since that time. Additionally, expanded hotel operations are expected to support the historic downtown area and enhance economic viability by bringing in revenues anticipated to come from out-of-town customers.

City Eligibility

Resolution 6954 outlines the City’s policy for establishing an NRA. City Policy Guidelines include:

· Typical Rebate Amounts & Duration

As per NRA policy, the City typically follows the below standard practice:

· Does not provide more than 50% rebate on incremental property taxes

· Does not establish an NRA for a period of time longer than 10 years

However, there is an exception provision within the policy which allows the City to “consider a greater rebate and/or a longer duration if sufficiently justified in the “but for” analysis.”[1]

· Cost-Benefit Ratio

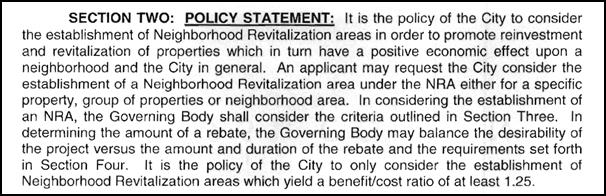

Resolution 6954, Section Two speaks to the cost-benefit ratio threshold. Specifically, the statement, “It is the policy of the City to only consider the establishment of Neighborhood Revitalization areas which yield a benefit/cost ratio of at least 1.25.”, indicates that for every $1 of cost incurred as a result of the project, $1.25 is received as benefit) for economic development projects.

|

|

From Resolution 6954, dated October 25, 2011.

City NRA Eligibility Criteria

For an NRA to be established, the project must not only meet statutory requirements, but also a majority of City policy criteria. The project meets City policy eligibility as detailed below:

|

City Policy: NRA Eligibility |

|||

|

City Policy Criteria |

When considering the establishment of a NRA, the City shall consider not only the statutory criteria, but if the project meets a majority of the below criteria: |

Eligible |

|

|

1 |

The opportunity to promote redevelopment activities which enhance downtown |

Y |

|

|

2 |

Provides the opportunity to promote redevelopment activities for properties which have been vacant or significantly underutilized. |

Y |

|

|

3 |

Provides the opportunity to attract unique retail and/or mixed use development which will enhance the economic climate of the City and diversify the economic base. |

Y |

|

|

4 |

Provides the opportunity to enhance neighborhood vitality as supported by the City's Comprehensive Plan or other sector planning document(s). |

Y |

|

|

5 |

Provides the opportunity to enhance community stability by supporting projects which embrace energy efficiency, multi-modal transportation options, or other elements of sustainable design. |

y |

|

|

Project must meet or exceed a 1:1.25 cost-benefit ratio. |

Y |

||

Conclusion—City Eligibility:

Staff believes the project as proposed will meet City NRA eligibility, meeting a majority of City policy criteria.

Industrial Revenue Bonds (IRB)

Industrial Revenue Bonds are an incentive established by the State of Kansas to enhance economic development and improve the quality of life. Considered a “conduit financing mechanism” whereby the City can assist companies in acquiring facilities, renovating structures, and purchasing machinery and equipment through bond issuance, IRBs can be useful to companies in obtaining favorable rate financing for their project, as well as providing a sales tax exemption on project construction materials.

IRBs are repayable solely by the company receiving them and place no financial risk on the City. When IRBs have been issued, the municipality owns the underlying asset and the debt is repaid through revenues earned on the property that has been financed by the bonds. If the company defaults, the bond owners cannot look to the city for payment.

IRB Eligibility

Project eligibility for IRB consideration is governed by both State (KSA 12-17,114 et seq.)[2] and City policy (Ordinance 8253). According to City policy, the City may from time to time grant IRBs when the project under consideration helps further economic and community development objectives. Additional eligibility criteria, as stipulated in the policy, are outlined below:

|

IRB: City Eligibility Criteria |

|||

|

Item # |

Policy Requirement |

Project Delivers |

Project Qualifies (Y/N) |

|

1 |

Only those projects which qualify under Kansas Law will be eligible for IRB financing. |

|

Y |

|

Proposed Project shall achieve one or more of the following public benefits: |

|||

|

2 |

2a: Meets economic goals of the City as set forth in policy and the Comprehensive Plan of Lawrence and Douglas County: |

||

|

Place high priority on retention and expansion of existing businesses. |

Expansion of existing business |

Y |

|

|

Encourage existing industry to expand. |

Expansion of existing business |

Y |

|

|

Assist new business start-ups |

N/A |

N |

|

|

Recruit new companies from out-of-state and internationally |

N/A |

N |

|

|

Encourage high technology and research based businesses. |

N/A |

N |

|

|

Encourage training and development of Lawrence area employees |

N/A |

N |

|

|

Encourage location and retention of businesses which are good "corporate citizens" that will add to the quality of life in Lawrence through their leadership and support of local civic and philanthropic organizations. |

The Eldridge has been a great corporate partner, supporting many local charities. Groups include the Old Fashioned Christmas Parade, Big Brothers Big Sisters, Cottonwood, LMH Endowment Association and others. |

Y |

|

|

2b: Promotes infill through the development of vacant lots, the rehabilitation of deteriorated properties or the adaptive reuse of historic properties. |

Project will replace long time vacant and unproductive lot (42 years) located along the community's historic downtown corridor, at 705 Massachusetts Street. |

Y |

|

|

2c: Enhance Downtown |

Project will replace vacant, unproductive lot with productive hotel space, enhancing the economic viability of downtown. |

Y |

|

|

2d: Incorporate environmentally sustainable elements into the design and operation of the facility |

Low-E coated insulated glass windows, florescent and LED lighting, use of environmentally safe cleaning products, recycling of glass, plastic, paper, tin and aluminum. To infill the vacant lot, which is currently gravel, will be an environmentally positive impact on the downtown area and adjacent neighboring properties: removing gravel, which can’t be maintained or cleaned properly in a downtown environment is a positive outcome. Expansion will allow upgrading kitchen exhaust system to be more environmentally friendly. |

Y |

|

|

2e: Provide other public benefits to the community, particularly as set forth in the Comprehensive Plan of Lawrence and Douglas County. |

Increases net new revenue to the community through accommodating increased number of out-of-town visitors and their spending on lodging, food, shopping, and transportation. Increases tax revenues through retail sales tax, liquor tax, transient guest taxes, and gasoline purchases. Project will support an estimated 18 direct, net new jobs created: 2 with an average annual salary of $40,000, 3 with an average annual salary of $35,000, 1 with an average annual salary of $50,000, and 12 with an average salary of $29,120. |

Y |

|

|

3 |

Prospective tenant shall show the financial capacity to complete the proposed project and successfully market the bonds. |

Owners have successfully completed and continue operating two local boutique hotels in the community. Owners have indicated they are currently working on financing for the project. |

|

Continued

|

IRB: Other Considerations (Preferred) |

||||

|

Item # |

Policy Requirement |

Project Delivers |

Project Qualifies (Y/N) |

|

|

1 |

City looks more favorably upon projects that support the below targeted industries: |

|||

|

Life Sciences/Research |

N/A |

N |

||

|

Information Technology |

N/A |

N |

||

|

Aviation and Aerospace |

N/A |

N |

||

|

Value-Added Agriculture |

N/A |

N |

||

|

Light Manufacturing and Distribution |

N/A |

N |

||

|

2 |

The City favors issuing Industrial Revenue Bonds to projects that bring in new revenues from outside the community or enhance the local quality of life over projects that will primarily compete against other local firms. |

|||

|

Project anticipated to bring in new revenues from outside community: |

Expansion of historic and iconic Eldridge Hotel will bring in new retails sales from food/beverage sales, meeting/banquet room rental and hotel room rental. 95% of new revenues are anticipated to come from out-of-town visitors. |

Y |

||

|

Project enhances local quality of life: |

Expansion of iconic, historic Eldridge Hotel replaces a long-time vacant, unproductive lot with unique, revenue-generating space, supporting and enhancing the economy along the historic downtown corridor and the community at large. Majority of economic impact is through net new revenues from out-of-town visitors. Economic benefits include direct spending from visitors on entertainment, food and beverage, shopping. New revenues increase overall livability of Lawrence. Expansion will improve aesthetics of downtown, enhancing awareness of the historic corridor and hotel. |

Y |

||

|

IRB: Special Consideration for Retail Projects |

||||

|

Item # |

Policy Requirement |

Project Delivers |

Project Qualifies (Y/N) |

|

|

1 |

Applicant demonstrates that the project is exceptional and unique |

Expansion of historic and iconic Eldridge Hotel will bring in new retails sales from food/beverage sales, meeting/banquet room rental and hotel room rental. |

Y |

|

|

2 |

Project is likely to add to the retail base by attracting new retail sales or capturing sales that are leaking to other markets. |

Estimated 95% of retail sales will be from out-of-town visitors |

Y |

|

Conclusion—City Eligibility:

Staff believes the project as proposed will meet City IRB eligibility, meeting a majority of City policy criteria.

Analysis

Estimated fiscal impacts to taxing jurisdictions is examined through a cost-benefit analysis and project financial feasibility is examined through a “But For” analysis (pro forma), both of which are required by current NRA policy.

Cost-Benefit Analysis

Based on information received through the incentives application, staff conducted analysis of the costs and benefits associated with the project utilizing the City’s economic development cost-benefit model. This model measures estimated fiscal impacts to four taxing jurisdictions: City, County, School District, and State. Furthermore, the model outputs a ratio reflecting the comparison of estimated costs to estimated benefits returned to the jurisdictions as a result of the project.

Assumptions utilized within the model:

· Capital Investment & Job Creation

According to the incentives application received, approximately $12.5 million will be invested in developing the property. Once redeveloped, the project is expected to support 18 new, full-time jobs anticipated to have an average annual salary of $32,469.

|

705 Massachusetts Street: Projected Employment |

|

|

# FT Jobs |

Average Annual Earnings |

|

2 |

$40,000 |

|

3 |

$35,000 |

|

1 |

$50,000 |

|

12 |

$29,120 |

|

18 |

$32,469 |

Although the model does not consider part-time or temporary positions, the applicant has indicated that the project will also support 3-5 construction jobs (at an annual estimated salary of $40,000) during the construction period and an additional 10-15 part-time positions during operations.

· Occupancy Rates

Hotel room occupancy assumptions were provided by the applicant and are shown below:

|

Hotel Rooms Estimated Occupancy |

|

|

Operational Year |

Occupancy Rate |

|

Year 1 |

57% |

|

Year 2 |

59% |

|

Year 3 |

61% |

|

Year 4 |

63% |

|

Year 5 |

65% |

|

Year 6 |

67% |

|

Year 7-20 |

69% |

Occupancy levels projected by the applicant are conservative as compared to national-level data. According to the most recent lodging data from the Price Waterhouse Cooper Real Estate Investor Survey (Q3-2014), occupancy rates for full-service hotels are expected to range between 66.1% and 73.6%.

For a historic perspective, the Lawrence Convention and Visitors Bureau reports historic occupancy rates for local, full-service luxury hotels averaged 60% over the past ten years (2005-2014), with rates ranging from a low of 43% during the economic downturn, to a high of 77% during pre-recession years.

· Net New Sales Taxes

Given the nature of the hotel business, it is reasonable to assume that some level of net new retail sales will be realized from hotel guests coming from outside the community. The applicant indicated approximately 95% of all revenues generated by the project will come from non-local sources.

For a more conservative perspective, staff assumed that 80% of sales tax revenues generated from meeting/banquet rooms, hotel rooms, and retail sales on food or other products sold at the hotel would be generated from out-of-town visitors.

Below shows estimated cumulative sales tax revenues generated to each taxing jurisdiction[3] assuming 80% of sales subject to sales tax comes from non-local consumers.

|

Sales Taxes Cumulative Total (est.) |

|||

|

Jurisdiction |

10 Years (2017-2026) |

15 Years (2017-2031) |

20 Years (2017-2026 |

|

City (1.55%) |

$324,128 |

$521,012 |

$738,389 |

|

County (1%) |

$209,115 |

$336,137 |

$476,380 |

|

State (6.5%) |

$1,286,057 |

$2,067,243 |

$2,929,736 |

|

Total |

$1,819,300 |

$2,924,393 |

$4,144,504 |

· Guest Taxes

The City imposes a 6% guest tax on hotel room rentals. This revenue is primarily used for tourist marketing purposes, and as such, helps promote the local lodging industry. Although these revenues were not incorporated into the cost-benefit analysis, estimated guest tax revenues are shown below, based on occupancy assumptions provided by the applicant.

|

Guest Taxes Cumulative Total (est.) |

|||

|

Jurisdiction |

10 Years (2017-2026) |

15 Years (2017-2031) |

20 Years (2017-2026 |

|

City (6%) |

$1,568,362 |

$2,521,028 |

$3,572,849 |

Property Taxes

In its present condition, the property generates approximately $4,900 per year in real property taxes. Under the NRA program, these “base” property taxes are shielded from rebates and would continue to be paid by the property owner. Only a percentage of the incremental increase in property value resulting from project improvements is subject to NRA rebates and then only during the NRA period. After the NRA period, no reimbursements are made on property taxes and the property returns fully to the tax rolls.

|

705 Mass. Street Tax History |

|||||||

|

Year |

Appraised |

Assessed |

Total Tax |

||||

|

Land |

Improvements |

Total |

Land |

Improvements |

Total |

||

|

2015 |

$315,560 |

$0 |

$315,560 |

$37,867 |

$0 |

$37,867 |

$4,922 |

|

2014 |

$315,560 |

$0 |

$315,560 |

$37,867 |

$0 |

$37,867 |

$4,913 |

After project completion, anticipated annual tax revenues received from the developer for the first year of operations is shown below. As can be seen, with a 15-year, 95% NRA, the owner/developer will pay over double what the property is currently producing in property tax revenues.

|

Estimated Tax Paid by Developer: Operations Year 1 (15-Year, 95% NRA) |

|

|

|

2017 |

|

Base Taxes |

$4,942 |

|

Incremental Taxes (5% of improved value) |

$6,070 |

|

Total Taxes Due |

$11,012 |

The following table provides a summary of the estimated base and incremental tax amounts the developer would be responsible for over time, given a 15-year, 95% NRA provided by all taxing jurisdictions. Note that under any of these scenarios, the estimated tax paid with an NRA more than doubles the current property tax collections.

|

Estimated Tax Paid from Owner Over Time (15-Year, 95% NRA Rebate) |

|||

|

|

During first 10 Years of Operations (2017-2026) |

During 15-Year NRA Period (2017-2031) |

During 20 Year Evaluation Period (2017-2036) |

|

Base Taxes |

$49,864 |

$75,169 |

$100,727 |

|

Incremental Taxes (5% of improved value) |

$67,087 |

$106,526 |

$986,080 |

|

Total Taxes Due |

$116,952 |

$181,696 |

$1,086,806 |

· Model Evaluation Period

For projects contributing to traditional economic development goals (i.e. primary job creation, high wage jobs, capital investment infusion) the model evaluation period has typically been 15 years. However, in projects that do not have traditional economic goals as their primary community contribution or projects that provide substantial intangible benefits, which would not be considered within the model (e.g. affordable housing), a longer evaluation period may be appropriate.

Results of a 15-year, 95% NRA are shown for both a 15-year and 20-year evaluation period. In general, the shorter the model evaluation period, the lower the cost-benefit ratios will be for the taxing jurisdictions.

Cost-Benefit Model Results:

Several cost benefit scenarios were ran utilizing information provided on the incentives application. Staff ran scenarios utilizing both a 15 and 20 year evaluation period with results shown below.

· 20 Year Evaluation Period

The following shows model results for a 20 year evaluation period. Note these model results do not include anticipated sales tax revenues. As can be seen, the project exceeds the 1.25 cost-benefit ratio for all taxing jurisdictions for a 10-, 12-, or 15-year NRA rebate period.

|

705 Massachusetts Street (20 Year Evaluation Period) |

|||||

|

Incentive Package |

City |

County |

USD 497 |

State |

Total Package Value |

|

15Y-95% NRA + IRB Sales Tax Exemption (20Y Evaluation Period) |

1.55 |

1.33 |

9.42 |

n/a |

$2,464,892 |

|

12Y-95% NRA + IRB Sales Tax Exemption (20Y Evaluation Period) |

1.65 |

1.52 |

11.48 |

n/a |

$2,005,530 |

|

10Y-95% NRA + IRB Sales Tax Exemption (20Y Evaluation Period) |

1.71 |

1.66 |

12.97 |

n/a |

$1,715,550 |

State does not have any costs.

The below table shows ratio results for the requested 15-year, 95% NRA with the addition of sales tax revenues (no guest tax revenues). As can be seen, with the addition of sales tax revenues, model result increase for both the City and County. School District ratios are unaffected as that taxing jurisdiction does not receive sales tax proceeds.

|

Including Sales Tax Revenues: 705 Massachusetts Street (20 Year Evaluation Period) |

|||||

|

Incentive Package |

City |

County |

USD 497 |

State |

Total Package Value |

|

15Y-95% NRA + IRB Sales Tax Exemption (20Y Evaluation Period) |

2.32 |

2.12 |

9.42 |

n/a |

$2,464,892 |

Assumes 80% of sales tax revenues are net new. State does not have any costs.

· 15 Year Evaluation Period

The following shows model results for a 15 year evaluation period. Note these model results do not include anticipated sales tax revenues. As can be seen, the project exceeds the 1.25 cost-benefit ratio for all taxing jurisdictions for a 10-, 12-, or 15-year NRA rebate period, with the exception of the County. Under this scenario, the 15- and 12-year, 95% NRA plus IRB sales tax exemption for construction materials does not meet the 1.25 cost-benefit ratio for the County.

|

705 Massachusetts Street (15 Year Evaluation Period) |

|||||

|

Incentive Package |

City |

County |

USD 497 |

State |

Total Package Value |

|

15Y-95% NRA + IRB Sales Tax Exemption (15Y Evaluation Period) |

1.32 |

0.96 |

6.43 |

n/a |

$2,464,892 |

|

12Y-95% NRA + IRB Sales Tax Exemption (15Y Evaluation Period) |

1.42 |

1.17 |

8.86 |

n/a |

$2,005,530 |

|

10Y-95% NRA + IRB Sales Tax Exemption (15Y Evaluation Period) |

1.49 |

1.32 |

10.63 |

n/a |

$1,715,550 |

State does not have any costs.

The below table shows ratio results using a 15 year evaluation period for the requested 15-year, 95% NRA with the addition of sales tax revenues. As seen, with the addition of these tax revenues, model results increase for both the City and County, exceeding the cost benefit threshold for all taxing jurisdictions.

|

Including Sales Tax Revenues: 705 Massachusetts Street (15 Year Evaluation Period) |

|||||

|

Incentive Package |

City |

County |

USD 497 |

State |

Total Package Value |

|

15Y-95% NRA + IRB Sales Tax Exemption (15Y Evaluation Period) |

2.00 |

1.67 |

6.43 |

n/a |

$2,464,892 |

Assumes 80% of sales tax revenues are net new. State does not have any costs.

Conclusion—Model Results:

The cost-benefit ratio is met for the City under all scenarios for both a 10- or 15-year, 95% NRA rebate and an IRB sales tax exemption on construction materials.

The cost-benefit ratio for the County can be met for a 10- or 15-year, 95% NRA rebate and an IRB sales tax exemption on construction materials under all scenarios using a 20 year evaluation period. However, under a 15 year evaluation period, the ratio is met only for a 10-year, 95% NRA with IRB sales tax construction materials if sales tax revenues are not included. With the addition of sale tax revenues, the ratio can be met for the County for a 15-year, 95% NRA with IRB sales tax construction materials.

“But For” Analysis

In order to provide a NRA rebate, the City must be convinced that without public assistance, the project will not be financially feasible. Whether or not the project would proceed if incentives are unavailable speaks to the “but for” test; But for the incentives, the project would not proceed.

Although there is no definite way to know in advance if the project will or will not proceed if incentives are not provided, there are financial metrics that can be examined to get a reasonable perspective. Through examining developer’s pro forma and other financial documents, project cash flow and return rates can be compared with and without public assistance.

· Projected Cash Flow

The Owner provided estimated annual revenues and expenses for the project, which were used to project annual cash flow. Property valuation information was provided by Douglas County Appraiser’s Office and was used to project annual property taxes.

As a worst case scenario, cash flow was first analyzed assuming the expansion portion of the project was not able to realize efficiencies of scale with the existing hotel:

1. The below table shows cash flow results when incentives are not provided. Cash flow is negative in years 2017-2028 (first 12 years), with the project realizing positive cash flow in year 2029 and beyond. Cumulative cash flow over the 20 year evaluation period is -$1,656,084.

|

Cash Flow No Incentives: Eldridge Hotel Expansion |

||||||||||

|

Oper. Year |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

2026 |

|

Y1 |

Y2 |

Y3 |

Y4 |

Y5 |

Y6 |

Y7 |

Y8 |

Y9 |

Y10 |

|

|

After Tax |

($399,469) |

($388,777) |

($356,516) |

($322,087) |

($285,429) |

($246,482) |

($205,182) |

($172,581) |

($139,333) |

($105,426) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash Flow No Incentives: Eldridge Hotel Expansion |

||||||||||

|

Oper. Year |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

2033 |

2034 |

2035 |

2036 |

|

Y11 |

Y12 |

Y13 |

Y14 |

Y15 |

Y16 |

Y17 |

Y18 |

Y19 |

Y20 |

|

|

After Tax |

($70,848) |

($35,585) |

$378 |

$37,053 |

$74,454 |

$112,596 |

$151,495 |

$191,163 |

$231,618 |

$272,874 |

2. The below table shows cash flow results when requested incentives are provided (15-Y, 95% NRA with IRB sales tax exemption). Cash flow is negative (although less negative as compared to the no incentives scenario) in years 2017-2025 (first 9 years), with the project realizing positive cash flow in year 2026 and beyond. Cumulative cash flow over the 20 year evaluation period is $367,917.

|

Cash Flow with Incentives: Eldridge Hotel Expansion |

||||||||||

|

Oper. Year |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

2026 |

|

Y1 |

Y2 |

Y3 |

Y4 |

Y5 |

Y6 |

Y7 |

Y8 |

Y9 |

Y10 |

|

|

After Tax |

($284,132) |

($270,900) |

($236,043) |

($198,960) |

($159,591) |

($117,872) |

($73,740) |

($38,243) |

($2,037) |

$34,894 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash Flow with Incentives: Eldridge Hotel Expansion |

||||||||||

|

Oper. Year |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

2033 |

2034 |

2035 |

2036 |

|

Y11 |

Y12 |

Y13 |

Y14 |

Y15 |

Y16 |

Y17 |

Y18 |

Y19 |

Y20 |

|

|

After Tax |

$72,563 |

$110,985 |

$150,175 |

$190,149 |

$230,922 |

$112,596 |

$151,495 |

$191,163 |

$231,618 |

$272,874 |

As a best case scenario, cash flow was then analyzed assuming the expansion portion of the project could realize cost savings through sharing efficiencies of scale with the existing hotel:

3. The below table shows cash flow results when incentives are not provided. Cash flow is negative in years 2017-2020 (first 4 years), with the project realizing positive cash flow in year 2021 and beyond. Cumulative cash flow over the 20 year evaluation period is $5,743,567.

|

Cash Flow No Incentives: Eldridge Hotel Expansion |

|||||||||

|

Oper. Year |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2025 |

2026 |

|

Y1 |

Y2 |

Y3 |

Y4 |

Y5 |

Y6 |

Y7 |

Y9 |

Y10 |

|

|

After Tax |

($120,760) |

($96,115) |

($51,262) |

($3,937) |

$45,927 |

$98,400 |

$153,555 |

$229,767 |

$269,011 |

|

|

|

|

|

|

|

|

|

|

|

|

Cash Flow No Incentives: Eldridge Hotel Expansion |

|||||||||

|

Oper. Year |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

2033 |

2035 |

2036 |

|

Y11 |

Y12 |

Y13 |

Y14 |

Y15 |

Y16 |

Y17 |

Y19 |

Y20 |

|

|

After Tax |

$309,033 |

$349,850 |

$391,476 |

$433,928 |

$477,222 |

$521,375 |

$566,404 |

$659,160 |

$706,922 |

4. The below table shows cash flow results when requested incentives are provided (15-Y, 95% NRA with IRB sales tax exemption). Cash flow is negative in year 2017 (year 1), but the project reaches positive cash flow in year 2018 (year 2) and beyond. Cumulative cash flow over the total evaluation period is $7,767,569.

|

Cash Flow with Incentives: Eldridge Hotel Expansion |

||||||||||

|

Oper. Year |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

2026 |

|

Y1 |

Y2 |

Y3 |

Y4 |

Y5 |

Y6 |

Y7 |

Y8 |

Y9 |

Y10 |

|

|

After Tax |

($5,423) |

$21,762 |

$69,212 |

$119,189 |

$171,765 |

$227,010 |

$284,998 |

$325,624 |

$367,063 |

$409,331 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash Flow with Incentives: Eldridge Hotel Expansion |

||||||||||

|

Oper. Year |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

2033 |

2034 |

2035 |

2036 |

|

Y11 |

Y12 |

Y13 |

Y14 |

Y15 |

Y16 |

Y17 |

Y18 |

Y19 |

Y20 |

|

|

After Tax |

$452,444 |

$496,419 |

$541,273 |

$587,024 |

$633,690 |

$521,375 |

$566,404 |

$612,327 |

$659,160 |

$706,922 |

Assuming the worst case scenario is represented by the project not realizing cost reductions from efficiencies of scale and the best case scenario was represented by the project realizing all cost reductions due to efficiencies of scale, cash flow was then examined for the average of these two projections.

5. The below tables shows cash flow results when averaged between best and worst case projections.

Without incentives, cash flow is negative in years 2017-2023 (first 7 years), with the project realizing positive cash flow in year 2024 and beyond. Cumulative cash flow over the 20 year evaluation period is $2,043,742.

|

Average No Incentives |

||||||||||

|

Cash Flow with Incentives: Eldridge Hotel Expansion |

||||||||||

|

Oper. Year |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

2026 |

|

|

Y1 |

Y2 |

Y3 |

Y4 |

Y5 |

Y6 |

Y7 |

Y8 |

Y9 |

Y10 |

|

After Tax |

($260,115) |

($242,446) |

($203,889) |

($163,012) |

($119,751) |

($74,041) |

($25,814) |

$9,353 |

$45,217 |

$81,792 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash Flow with Incentives: Eldridge Hotel Expansion |

||||||||||

|

Oper. Year |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

2033 |

2034 |

2035 |

2036 |

|

|

Y11 |

Y12 |

Y13 |

Y14 |

Y15 |

Y16 |

Y17 |

Y18 |

Y19 |

Y20 |

|

After Tax |

$119,093 |

$157,133 |

$195,927 |

$235,490 |

$275,838 |

$316,986 |

$358,949 |

$401,745 |

$445,389 |

$489,898 |

With incentives, cash flow is negative in years 2017-2020 (first 4 years), with the project realizing positive cash flow in year 2021 and beyond. Cumulative cash flow over the 20 year evaluation period is $4,067,743.

|

Average with Incentives |

||||||||||

|

Cash Flow with Incentives: Eldridge Hotel Expansion (15Y NRA) |

||||||||||

|

Oper. Year |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

2026 |

|

Y1 |

Y2 |

Y3 |

Y4 |

Y5 |

Y6 |

Y7 |

Y8 |

Y9 |

Y10 |

|

|

After Tax |

($144,778) |

($124,569) |

($83,416) |

($39,885) |

$6,087 |

$54,569 |

$105,629 |

$143,691 |

$182,513 |

$222,112 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash Flow with Incentives: Eldridge Hotel Expansion (15Y NRA) |

||||||||||

|

Oper. Year |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

2033 |

2034 |

2035 |

2036 |

|

Y11 |

Y12 |

Y13 |

Y14 |

Y15 |

Y16 |

Y17 |

Y18 |

Y19 |

Y20 |

|

|

After Tax |

$262,503 |

$303,702 |

$345,724 |

$388,587 |

$432,306 |

$316,986 |

$358,949 |

$401,745 |

$445,389 |

$489,898 |

Conclusion: Cash Flow

In examining the averaged cash flow scenarios, it is reasonable to assume the project would not be feasible without public support. If incentives are not provided, analysis shows a negative cash flow during the first 7 years. When cash flow is examined over time, returns are negative (-$952,706) during the first 10 years, with positive net returns of only $30,774 over a 15-year period.

Even with incentives provided at a 15-Y, 95% rebate level, cash flow is negative during the first 4 years. When cash flow is examined over time, returns are positive over both a 10- and 5-year time period with returns of $321,954 during the first 10 years, and returns of $2,054,776 over a 15-year period.

NRA Duration

Although the need for public support is evident, the duration period for the NRA is not as apparent. The cost difference between providing a 10-year, 95% NRA as compared to a 15-year, 95% NRA is shown below.

|

Difference in Cash Flow by NRA Term |

||||

|

Average Cash Flow with Incentives |

10 Years (2017-2026) |

15 Years (2017-2031) |

||

|

10Y NRA: Average Cash Flow: With Incentives |

$321,954 |

$1,305,434 |

||

|

15Y NRA: Average Cash Flow: With Incentives |

$321,954 |

$2,054,776 |

||

|

Difference |

|

|

$0 |

$749,341 |

For comparison, below shows taxes paid by owner for both a 10- and 15-year NRA.

|

Estimated Tax Paid from Owner: 15-Year, 95% NRA Rebate |

||||

|

|

During first Year of Operations (2017) |

During first 10 Years of Operations (2017-2026) |

During 15-Year NRA Period (2017-2031) |

During 20 Year Evaluation Period (2017-2036) |

|

Base Taxes |

$4,942 |

$49,864 |

$75,169 |

$100,727 |

|

Incremental Taxes (5% of improved value) |

$6,070 |

$67,087 |

$106,526 |

$986,080 |

|

Total Taxes Due |

$11,012 |

$116,952 |

$181,696 |

$1,086,806 |

|

|

|

|

|

|

|

Estimated Tax Paid from Owner: 10-Year, 95% NRA Rebate |

||||

|

|

During first Year of Operations (2017) |

During first 10 Years of Operations (2017-2026) |

During 15-Year NRA Period (2017-2031) |

During 20 Year Evaluation Period (2017-2036) |

|

Base Taxes |

$4,942 |

$49,864 |

$75,169 |

$100,727 |

|

Incremental Taxes (5% of improved value) |

$6,070 |

$67,087 |

$855,867.74 |

$1,735,421 |

|

Total Taxes Due |

$11,012 |

$116,952 |

$931,037 |

$1,836,148 |

The NRA duration period should be a topic of discussion for PIRC and the governing bodies.

· Return Rates

One common financial metric that can be examined for project feasibility is the Internal Rate of Return (IRR). The IRR is a complex formula that takes into consideration annualized compounded return rates based on the project’s anticipated operating expenses and revenues over time, as well as recapture returns from selling the property at the end of a holding period. The IRR a developer requires to proceed is subjective and depends on various factors, including shareholder demand for returns, investment goals, availability of alternate projects and comparative potential returns, and many other financial and investor considerations.

Since the IRR assumes the hypothetical sale of the property at some time in the future and this project represents only a portion of the total hotel property and its proportional income, review of the IRR for the entire project (existing hotel + expansion) would be necessary to evaluate potential investor returns. Therefore, IRR review under these circumstances was beyond the scope of this report and not examined.

Conclusion—But For Test

After examining cash flow scenarios, Staff believes it is reasonable to assume the project would not proceed without public assistance. However, it is not as apparent what the duration should be for the NRA rebate period. The NRA duration period should be a topic of discussion for PIRC and the governing bodies. Additional topics such as taxes paid over time, revenues generated for taxing jurisdictions and other considerations (see following) may want to be taken into consideration when discussing the NRA duration period.

Other Considerations

Other non-quantifiable project benefits and impacts should also be considered within the context of this request, including:

· Project provides an opportunity to replace an unproductive vacant lot with productive space. Records indicate the lot at 705 Massachusetts has been vacant since 1973 (42 years).

· Project provides an opportunity to promote increased visitor traffic in support of Downtown Lawrence.

· Project provides an opportunity to support downtown, infill development along the historic downtown corridor.

· Past public support for the existing Eldridge Hotel included a 10-year tax abatement (3% real property, 97% personal property) and Industrial Revenue Bond Financing authorized in 1986. See Appendix C for additional information.

· The expansion project will not provide on-site parking to accommodate additional guests. However, the downtown zoning district where the project will be located does not require redevelopment to provide off-street parking. Regardless of parking requirements, demand for parking will likely be impacted and the parking impact of the project, both during and after construction, should be considered.

For background information, the below shows parking provided for some of the more recent developments that received public incentives.

|

Incentivized Projects |

|

|||

|

Project |

Project Provided Private Parking |

On-Site Parking Required |

Notes |

|

|

NRA: 8th and Pennsylvania District, 720 E 9th St. |

Y |

Y |

37 provided/28 required |

|

|

NRA: 1040 Vermont (Treanor Headquarters) |

Y |

N |

Also relies on public parking |

CD |

|

NRA: 810/812 Pennsylvania (Cider Building) |

N |

Y |

Utilizes provision of shared off-site parking in meeting Development Code. |

|

|

NRA: 1106 Rhode Island St. (Hernly Associates) |

Y |

Y |

|

|

|

NRA: 1101/1115 Indiana St. (HERE Kansas) |

Y |

Y |

May rely on some KU parking spaces, but not City parking spaces |

|

|

NRA: 900 Delaware St. (9 Del Lofts) |

Y |

Y |

60 provided/72 required, variance granted. Eventually can use proposed lot on NW corner of 9th & Delaware. |

|

|

NRA: 1001 Massachusetts (Masonic Temple) |

N |

N |

|

CD |

|

TIF: The Oread |

Y |

Y |

182 provided/320 required, variance granted |

|

|

TIF: 9th & New Hampshire: South Project |

Y |

Y |

Garage |

CD |

|

TIF: 9th & New Hampshire: North Project |

Y |

Y |

Garage |

CD |

City of Lawrence, Planning Department. The Development Code does not require that developments provide on-site parking in the CD (Downtown Commercial) zoning district.

Performance Agreement

Per City policy, the property owner/development team would be required to enter into a performance agreement with the City in order to receive NRA rebates. The most significant reason for this is to make sure the developer coordinates with the City and County at the beginning of the establishment of the district and to ensure that there are no delinquent property taxes during any of the years of the NRA plan. In addition, performance provisions could be stipulated within the agreement (e.g. start and end of construction, compliance with land use requirements).

Staff Recommendation

The 1.25 ratio threshold is exceeded for the City for a 10-year and 15-year, 95% NRA with IRB sales tax exemption on construction materials under all scenarios (15- or 20-year evaluation period, with and without sales tax revenues included). The ratio threshold is met for the County for the same incentive package under all scenarios, with the exception of the 15 year evaluation period when sales tax revenues are excluded.

The current zoning district does not require projects redeveloped in downtown to provide off-street parking as would be the case in other zoning areas. However, since the project will not provide off-street parking, there likely will be some increased demand on existing parking space. The impact on existing businesses in the downtown corridor should be discussed when considering the NRA duration. In cases where off-street parking is provided, it may be appropriate to provide a longer NRA duration.

The duration period for the NRA should be a topic of discussion for PIRC and the governing bodies.

Should an incentive package be approved, Staff would recommend including the following provisions in a performance agreement:

· Condition any incentives authorized for the project on the complete compliance with all land use requirements for the property, including the City’s historic and downtown design guidelines. Failure to comply with these requirements would nullify any incentives approved.

· Project construction to commence within one year and end within two years of incentives approval.

PIRC Requested Action

Public Incentives Review Committee to provide recommendation on participation in a NRA for 705 Massachusetts Street, including duration and percentage rebate level, and for an IRB sales tax exemption on construction materials.

Addendum B: Additional Cost-Benefit Model Scenarios

|

705 Massachusetts Street (20 Year Evaluation Period) |

|||||

|

Incentive Package |

City |

County |

USD 497 |

State |

Total Package Value |

|

15-Year, 85% NRA + IRB Sales Tax Exemption (20Y Evaluation Period) |

1.61 |

1.45 |

10.76 |

n/a |

$2,251,839 |

|

12-Year, 85% NRA + IRB Sales Tax Exemption (20Y Evaluation Period) |

1.70 |

1.62 |

12.60 |

n/a |

$1,840,831 |

|

10-Year, 85% NRA + IRB Sales Tax Exemption (20Y Evaluation Period) |

1.75 |

1.74 |

13.94 |

n/a |

$1,581,375 |

|

CBA did not consider guest tax revenues or retail sales tax revenues generated. |

|||||

|

705 Massachusetts Street (15 Year Evaluation Period) |

|||||

|

Incentive Package |

City |

County |

USD 497 |

State |

Total Package Value |

|

15-Year, 85% NRA + IRB Sales Tax Exemption (15Y Evaluation Period) |

1.38 |

1.10 |

8.01 |

n/a |

$2,251,839 |

|

12-Year, 85% NRA + IRB Sales Tax Exemption (15Y Evaluation Period) |

1.47 |

1.28 |

10.19 |

n/a |

$1,840,831 |

|

10-Year, 55% NRA + IRB Sales Tax Exemption (15Y Evaluation Period) |

1.54 |

1.42 |

11.78 |

n/a |

$1,581,375 |

|

CBA did not consider guest tax revenues or retail sales tax revenues generated. |

|||||

Addendum C: Historic account of public assistance for existing Eldridge Hotel

On October 1, 1985, The City Commission received a letter from Rob Phillips requesting a public hearing to consider a letter of Intent to issue $2,000,000 in Industrial Revenue Bonds for the purpose of renovating the Eldridge House. During the public hearing held on October 22, 1985, the City Commission unanimously approved a motion to require $1,000,000 in private investment capital be raised before issuance of the IRBs. The Commission adopted a Resolution of Intent (Res No. 4882) to issue $2,000,000 in IRBs for Eldridge House Investors L.P., which was amended to include the private capital investment requirement.

The first and second readings of Ordinance No. 5723 authorizing the issuance of the bonds were done at the August 19 and 26th, 1986 City Commission meetings. Rob Phillips, representing Eldridge Hotel Investors Limited Partnership stated that the in-lieu-of-tax payment would be $10,000 more than current taxes. Ordinance 5723 was approved 5-0 supporting bond issuance for the project and executed on August 26, 1986.

IRBs (Series of August 1, 1986) were issued for $2,000,000 for the Eldridge House Project on behalf of Eldridge House Investors L.P. (Rob Phillips, general partner; Edward Seyfert, original limited partner).

In association with the IRBs, there was 10-year tax abatement (3% on real property, 97% on personal property) from 1-1-1987 through 12-31-1996. No jobs were estimated to be created as a result of the abatement. Under terms of a separate agreement, the tenant covenanted and agreed to an annual payment-in-lieu of taxes in the amount of $25,934.20 for the period of the exemption.

Addendum D: About the Cost-Benefit Model

The City of Lawrence uses a proprietary Cost-Benefit model when examining projects. The Cost-Benefit model is one tool that government decision makers can incorporate in their decision-making process. The City’s cost-benefit model provides a framework for estimating the fiscal impacts of a project, assuming it were in existence and in use today, through the examination of costs and benefits to various taxing jurisdictions (City, County, School District, State). As with all economic models, there are limitations, which are generalized below:

· Does not consider intangible effects

The model does not speak to the effects of intangible costs or benefits resulting from a project, since intangible effects are difficult, if not impossible to assign a dollar value.

· Does not consider private or market effects

The model only seeks to quantify the cumulative effect on public revenues and expenses and not the effect on private interests that may be affected by a project. Thus, the model only considers public, or governmental, costs and revenues.

Logic would dictate that any development may also have a financial impact on the private sector. For example, if one were analyzing a proposal to build a new baseball stadium, the new tax revenue from the building and property – as well as the costs for providing additional public security and emergency services (police, fire, ambulance, etc.) – would factor into the analysis. However, the effect of the stadium on neighboring property values or the impact on business at local restaurants would not be accounted for within the model.

The cost-benefit model does not consider market impacts of a project, including the amount of market share a project captures from existing businesses or the amount of new revenues brought into the community as a direct result of a project. A market study can be employed to study these effects.

· The model considers direct effect economic impacts

Multipliers used within the model are applied to direct effects such as the number of jobs created by the project and associated wages. The model does not attempt to measure all indirect effects such as capturing visitor spending associated with a project, nor the economic effects of that spending as outside dollars circulate through the community over time.

· Model assumes current effects

The model is run on assumptions and estimations provided at the time of analysis. The current effects aspect of the model means that the analysis provides a means of estimating the financial impact of a development as if the project under consideration were in existence and in use today, given estimated costs and assumptions that are usually defined prior to the project being constructed or operational. Given that it may be difficult to predict future costs and benefits accurately, there is an implicit assumption that future changes affect both revenues and costs.

In addition, the model does not reflect any changes in economic adjustments over time due to macroeconomic conditions, regional industrial structure, public policies, and technological advances.

· Does not consider fiscal impacts of temporary or part-time employment

Employment analyzed is for full-time, permanent positions related to a project and does not consider temporary jobs created due to project construction or part-time positions created during project operation.

Other considerations for decision making:

There could be several important considerations that fall outside of the realm of municipal budgets and cost-benefit analysis. For example, fiscal impacts of development on abutters, local businesses and natural resources are not accounted for in cost-benefit analysis.

Cost-benefit analysis also does not consider issues of equity and social responsibility. For instance, while it may be easy to identify the fiscal downsides of low-income housing on municipal and school budgets, municipalities may also bear some level of responsibility for ensuring access to affordable housing. Finally, communities maintain certain values that cannot be assigned a price tag, such as the intrinsic value of nature, cultural heritage, and aesthetics.

Depending on the project, it may be prudent to employ other analytical models or studies (e.g. economic impact analysis; pro forma/but-for analysis; trade area analysis; tourism impact, market demand and other studies; etc.) in conjunction with cost-benefit analysis, as well as give consideration to other, non-quantifiable elements to gain insight into a project’s overall value to the community.

Addendum E: Projected Property and Sales Tax Revenues